How to analyse and reduce bank fees in five steps

By Orsolya Kozák, Treasury Specialist – Customer Success

Bank fee management is one of those treasury tasks that gets pushed to the bottom of the list. It’s not urgent. It doesn’t have a deadline. And if you’ve never done a proper analysis, you don’t know what you’re missing – which is exactly the problem.

As a corporate treasurer, I’ve been here before. The first time I managed bank fees properly, I didn’t really know what I was doing. By the time I did it again, I did. The difference in what I found – and what I was able to save – was significant. So here’s what I’d tell anyone starting out.

Step 1: Collect the files from your banks

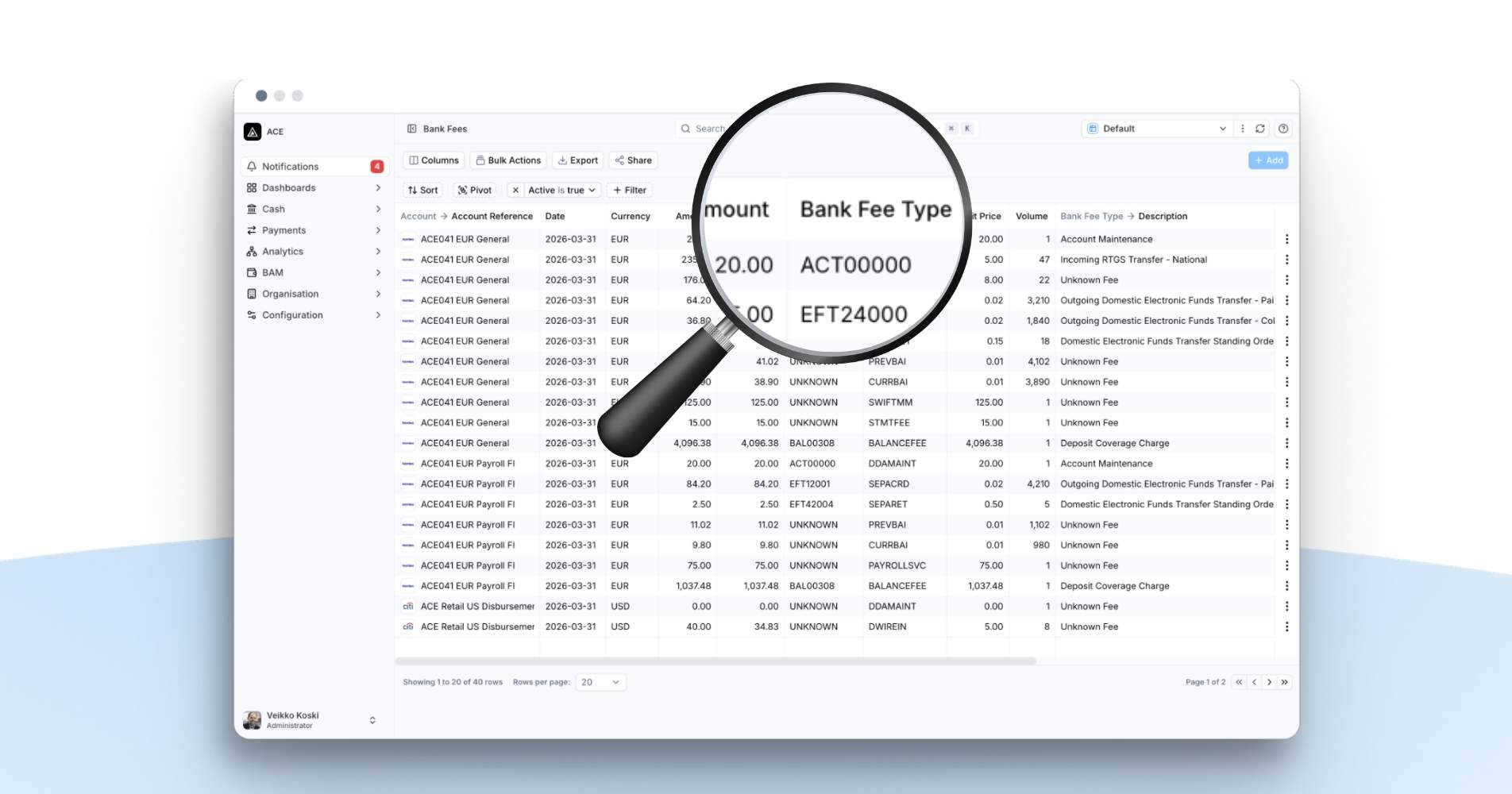

Banks provide fee statements in different formats, and the format you’ll receive depends on where your banks are based. In the US, the standard is EDI 822. In Europe and other regions, standard formats include camt.086, TWIST BSB, and proprietary PDF. Formats can also vary by bank and by the nature of your relationship with them.

Some banks will send you a structured file. Others will send you a PDF, which makes analysis tricky. Some will send CSV if you ask them nicely and give them a template to work from.

The first practical task is to agree a format with each of your banking partners and actually get the files. If you have 10 banking relationships, expect this to take longer than you’d like. There’s usually a turnaround time, so build this into your process.

Step 2: Standardise the categories

Once you have the files, you’ll quickly notice that every bank has its own naming conventions. One bank calls it “SEPA credit transfer.” Another calls it “outgoing SEPA.” Another has three subcategories for what is, functionally, the same transaction type.

Before you can compare anything, you need to map each bank’s codes and descriptions to a consistent set of categories. Payment, maintenance, account management, value-added services – whatever structure makes sense for your organisation. This step requires some patience, but it’s the foundation for everything that follows.

Without standardised categories, you’re not comparing like with like, and your analysis won’t hold up when you take it to a banking relationship manager.

Step 3: Run the analysis

With clean, categorised data, you can start asking useful questions.

The most obvious one: how much are you paying per bank, per category? If Bank A is charging significantly more than Bank B for equivalent SEPA transactions, that’s worth understanding. Maybe there’s a contractual reason. Maybe there isn’t. Either way, you now have the evidence to have that conversation.

Beyond cost comparison, look at what services you’re actually being charged for, and this is where it tends to get interesting. In my experience, many companies are paying for services they either don’t use or didn’t know they had.

A case in point: I once found a “warehouse” service on a bank fee statement, that was costing around €500 a month. After a helpful discussion with the bank, in which they explained what the service was for, we mutually decided that it was not needed. That’s exactly the kind of saving that would never have surfaced without sitting down and going through the data properly.

Go through every line. If you don’t recognise a service, ask the bank to explain it.

Step 4: Use the data to negotiate

Bank fee analysis is most powerful when it becomes part of your relationship management with your banking partners.

If you’re heading into a review meeting and you can say: “Last year we paid you X in fees across these categories” – that changes the dynamic. You’re not negotiating on instinct; you’re negotiating on fact. That’s particularly useful when you’re also factoring in the broader relationship – how much business you’re giving each bank across payments, FX, credit facilities – and making sure the balance is right.

The goal isn’t to squeeze every bank as hard as possible. A good analysis sometimes confirms that a relationship is fair and working well. That’s valuable to know too. What you’re really doing is creating visibility – so that decisions about banking relationships are made deliberately, rather than by default.

Step 5: Build in a regular cadence

Bank fees change. Services get added. Pricing gets updated. A one-off analysis is useful, but the real value comes from reviewing at a regular cadence – and from having the right infrastructure to make that practical without it becoming a manual burden each time. That’s something we’ve built into FinanceKey’s bank fees module for clients managing fees at scale.

The other piece that will matter increasingly is automated price list comparison: uploading your agreed tariff with each bank and having the system flag discrepancies against what you’re actually being charged. If your contract says €1 per cross-border payment and the statement shows €1.50, that’s recoverable. Banks do make errors, and most will issue a credit if you can point to the specific discrepancy.

Who should be doing this?

If you have more than around 100 bank accounts and three or more banking relationships, bank fee analysis is definitely worth doing.

If you’re managing a multinational treasury with entities across multiple countries, there’s an additional layer: visibility into what your local finance teams are doing with your banking partners. Bank fee data can give you a view of payment activity by country – something that often gets lost when treasury is centralised but operations are distributed.

The main thing is to start. The fees are there, the data is available, and most of it is just waiting to be looked at.

Where does your treasury sit on the journey from reactive to fully optimised? My colleague Macer Skeels sets out a useful framework in his article on why bank fees are the cost category most treasury teams are not managing.