How to automate cash sweeps and funding transfers in corporate treasury

Cash doesn’t move itself. In a corporate treasury with accounts spread across multiple banks and entities, cash sits idle in some places while other accounts run short. That mismatch has a cost – in borrowing, in foregone interest income, and in the time your team spends manually reviewing balances and initiating transfers.

Automating cash sweeps and funding transfers is how treasury teams fix this. This article explains the mechanics, the underlying structures (including cash pooling), and what genuine automation looks like compared to the alert-and-approve workflows most teams are still running.

What is cash sweeping?

Cash sweeping is the automated movement of funds between bank accounts, triggered by balance thresholds or scheduled rules. When an account exceeds a target balance, the excess is swept to a central account or investment vehicle. When an account falls below a minimum, funds are transferred in to restore it.

The underlying logic is simple: idle cash earns nothing, and overdrawn accounts cost money. Sweeping keeps balances within defined bands without requiring manual intervention each time.

There are two common sweep types:

Zero balancing – subsidiary account balances are swept to zero at the end of each day. All funds consolidate into a master account, typically held at the group or treasury level.

Target balancing – accounts are swept to or from a predefined target balance, rather than to zero. Useful where subsidiaries need a working buffer.

Both approaches serve the same goal: concentrating liquidity where it can be managed actively.

What is account funding?

Account funding is the reverse of sweeping – transferring money from a central account out to subsidiaries or operational accounts that need it. Together, sweeping (concentration) and funding (distribution) form a closed loop of liquidity management.

In practice, funding decisions are often reactive: a payment run is coming, an account is low, a transfer is needed. The question is whether your team is initiating that transfer manually, or whether the system is handling it based on defined rules.

Cash pooling: the structure behind the automation

To automate cash movements at scale, you need more than rules – you need a structure. That’s where cash pooling comes in.

Cash pooling is a liquidity management arrangement that lets organisations optimise cash across multiple bank accounts, treating group-level funds as a single pool rather than isolated balances. It’s what makes group-wide sweeping and funding operationally coherent rather than ad hoc.

There are three main types:

Physical cash pooling

Money actually moves between accounts. Subsidiary balances are swept into a master account (or funded from it) on a scheduled basis. Zero balancing is the most common form. The master account holds the net position; subsidiaries carry minimal or zero balances overnight.

Physical pooling gives the group complete control over consolidated cash. It also creates intercompany lending arrangements, which carry accounting and tax implications that need to be managed carefully.

Notional pooling

No money moves. Instead, the bank combines account balances virtually for the purpose of interest calculation. If one account holds €10m and another is €8m overdrawn, the bank calculates interest on the net €2m position – not on each account separately. The group pays interest on €2m rather than on €8m, which reduces borrowing costs significantly.

Notional pooling is operationally simpler than physical pooling, but it is increasingly restricted by some regulators and is not universally available across banks or jurisdictions.

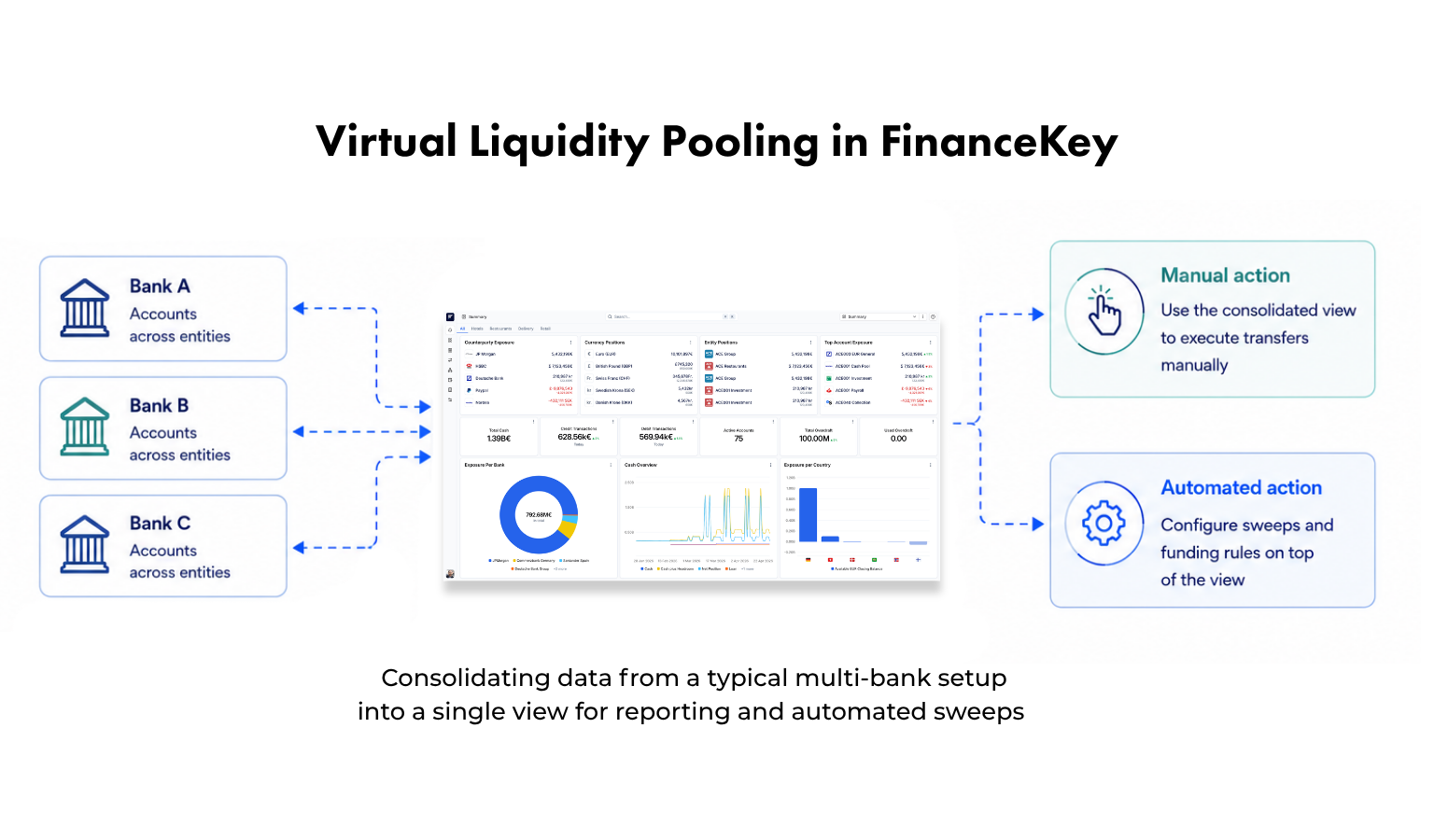

Virtual liquidity pools

A third type – less widely discussed but genuinely useful – is the virtual liquidity pool, sometimes called a positioning pool.

This is a data layer that combines balances into a single view, giving treasury teams a clear picture of their net liquidity position across accounts and entities.

What makes this more than a reporting tool is what it enables next. When software like FinanceKey provides a virtual liquidity layer, the visibility it creates is the foundation for action: treasury teams can use that consolidated view to execute transfers manually, or to configure automated sweeps and funding rules on top of it.

Critically, because the pool exists in the platform rather than at a bank, it can span multiple banking relationships – something bank-native cash pool structures, which are limited to accounts held at that bank, cannot do.

Why bank-native cash pools have limitations

Most banks offer physical or notional pooling as a product, but there are practical constraints.

Cost – setting up a cash pool at a bank typically involves significant implementation fees, and most banks charge a monthly maintenance fee on top. For smaller treasury operations or those with distributed banking relationships, this can make bank-native pooling uneconomical.

Single-bank scope – a bank’s pooling product works within its own infrastructure. If your accounts are spread across five banks – which is common for any company operating internationally – each bank can only pool its own accounts. You end up with multiple siloed pools rather than a single consolidated view.

Currency limitations – most bank pooling structures are single-currency. Running a multi-currency pool is something only the largest global and leading regional cash management banks offer natively. For groups that do not bank primarily with those institutions, or that need to span multiple banking relationships, this is a meaningful constraint. FinanceKey supports multi-currency pools regardless of which banks are involved.

What threshold-based sweeping looks like in practice

Whether you are running a formal cash pool or automating individual account pairs, the mechanics of sweeping work around thresholds and rules.

A typical rule set looks like this:

- Minimum balance: if the account falls below €50,000, fund it back to the target

- Target balance: the operating level for the account – say, €100,000

- Maximum balance: if the account exceeds €500,000, sweep the excess to the master account

- Trigger: real-time balance check, end-of-day run, or both.

In a manual treasury process, someone reviews balances each morning and initiates transfers that day. In an automated process, the system applies the rules continuously and executes transfers without human intervention.

The gap between those two states – monitoring versus acting – is where a lot of treasury teams sit. They have visibility, but not automation. Alerts fire, but someone still has to approve and initiate the transfer.

Why multi-bank automation is harder than it sounds

The reason most treasury automation remains manual or semi-manual is connectivity. Funding an account automatically means checking the balance in the account you’re paying from, then moving the cash into the account that needs it, all in one flow. That’s the hard part, because each bank has its own API, data format, and authentication requirements.

Traditional TMS platforms were designed around batch file exchange with banks – SWIFT messages, MT940 statements delivered once or twice a day. That model is compatible with end-of-day sweeping, but it cannot support real-time or intraday automation.

API-first bank connectivity changes this. With direct bank APIs, the treasury system can pull live balances at any moment and initiate payments without waiting for a scheduled file transfer. This is the foundation FinanceKey is built on, and it is what makes genuinely continuous sweeping possible – not just daily, but throughout the working day.

For groups banking across multiple institutions, the platform handles this connectivity bank by bank, abstracting away the differences in each bank’s API so that threshold rules can be applied consistently across the entire account structure.

Case study

Nors drives €1M+ in treasury savings through FinanceKey integration

FinanceKey offered Nors Group a flexible, scalable alternative to rigid bank-led solutions with auto-sweeping and real-time cash visibility.

What automation looks like

A fully automated cash sweep and funding workflow, built on real-time bank connectivity, looks something typically looks like this:

- The platform pulls live balances from all connected bank accounts

- Each balance is checked against the defined threshold rules for that account

- Where a rule is triggered, a transfer is initiated automatically – no human approval required for standard, in-policy movements

- The transfer is executed via the bank’s API

- The updated balance is reflected immediately in the treasury dashboard

Exceptions – unusual amounts, accounts outside normal parameters, bank connectivity failures – are flagged for human review

In this model, the treasury team’s role shifts from initiating routine transfers to setting the rules, reviewing exceptions, and refining the logic over time. The manual work is replaced by oversight.

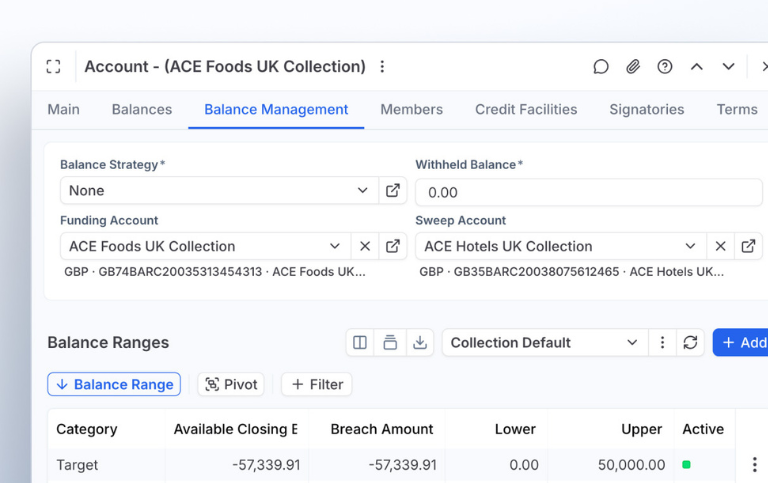

How FinanceKey automates cash sweeps and funding

FinanceKey connects directly to banks via API, providing real-time balance data across your full account structure – regardless of how many banks you work with or which currencies are involved.

Configuration

FinanceKey supports physical, notional, and virtual liquidity pool structures – configurable to reflect however a group’s treasury is actually organised:

- Bank-agnostic – pools can be configured across multiple banking relationships. Groups do not need all their accounts at one bank to benefit from pooling.

- Multi-currency – single and multi-currency configurations are supported natively, covering scenarios that most banks cannot accommodate without significant additional cost or complexity.

- Flexible hierarchy – configure a single pool aggregating all accounts, or a multi-level structure with subsidiary pools feeding into regional pools feeding into a group master, depending on your entity structure.

Capabilities

- Real-time balance monitoring – live balances pulled continuously from all connected bank accounts via direct API, across all banks in the structure.

- Threshold-based automation – define minimum, target, and maximum balances per account; transfers are triggered and executed automatically when thresholds are crossed.

- Manual or automated action – the consolidated net position view supports both manual transfer decisions and fully automated sweep and funding rules, depending on the treasury team’s preference or policy.

- Exception handling – out-of-policy movements are flagged for human review while routine transfers execute without intervention.

Getting started

The right starting point depends on where your treasury currently sits.

If you have no visibility across accounts, begin there. A positioning pool gives you a consolidated view of your net cash position without requiring you to change how money moves.

If you have visibility but transfers are still manual, the next step is defining your threshold rules and testing automated execution on a subset of accounts before rolling it out more broadly.

If you are managing multiple banks and finding that each one’s native pooling product only covers part of your needs and countries you operate, a bank-agnostic approach lets you bring the whole picture together.

Discover FinanceKey

Explore our solutions

Connectivity

Bring every financial system together

Bring your bank portals, ERPs and treasury systems together in one platform.

Cash visibility

Instant visibility into your cash position

Get real-time visibility into your bank balances and liquidity.

Run cash sweeps

Automate cash sweeps and account funding

Set threshold-based rules to move money between accounts.