Bank fees: the cost category most treasury teams are not managing

By Macer Skeels, CTO and Co-Founder, FinanceKey

Banks bill over the equivalent of $2.5 trillion in service charges each year.1 Most of those charges are paid without question. In most treasury environments, bank fees are reviewed infrequently, rarely connected to the activity driving them, and almost never benchmarked systematically against what peers are paying.

The result is a cost category that accumulates without scrutiny. Billing errors go unnoticed. Pricing drifts. Unused accounts and services persist because nobody has the data to challenge them and act.

The limiting factor is rarely willingness to analyse fees. It’s the absence of infrastructure that makes continuous analysis practical.

The data problem

Bank fee data is readily available, yet deeply fragmented. Across different banks, geographical regions, and legal entities, data structures vary widely between CAMT.086 XML, TWIST XML, and ANSI X12 822 EDI text. This structural variation is further complicated by inconsistent fee categorisation. Proprietary bank code sets routinely override industry standards like AFP and AFP Global.

The result is that even skilled treasury professionals miss material savings. Industry data consistently puts the proportion of bank fees billed in error at up to 5%,2 meaning a corporate paying $2m annually in bank charges may be absorbing $100k in errors that are not verified.

Without a unified view, treasury teams interpret fragmented snapshots rather than managing a coherent cost structure. Monthly or quarterly reviews miss gradual price increases and emerging inefficiencies. By the time anomalies surface, costs have already accumulated.

What continuous fee intelligence looks like

Done properly, bank fee intelligence replaces the quarterly spreadsheet exercise with something continuous and structured. This is what we built FinanceKey’s bank fees intelligence module to do.

Fee data is centralised and normalised automatically, converted to a single reporting currency, and mapped to AFP Global Service Codes so you have a consistent basis for benchmarking across your entire banking panel.

Billing errors surface in real time rather than months after the fact. Pricing drift, defined as the gradual increase in fees that occurs even when your volumes and account structures are unchanged, becomes visible and quantifiable. And when it is time to negotiate, you are no longer estimating, you have the line-by-line data to make the case.

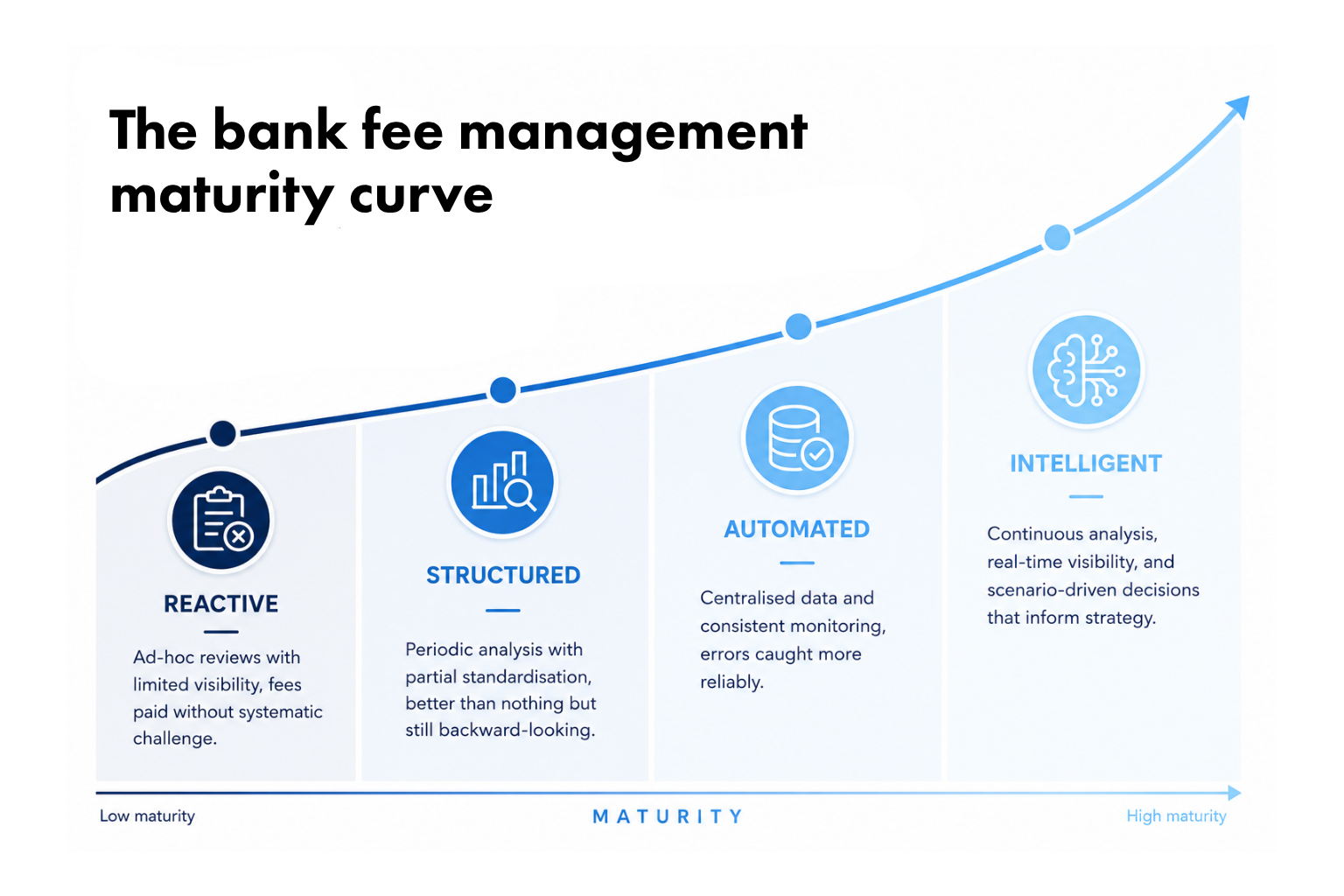

Most organisations evolve through four stages of bank fee management:

- Reactive – ad-hoc reviews with limited visibility, fees paid without systematic challenge

- Structured – periodic analysis with partial standardisation, better than nothing but still backward-looking

- Automated – centralised data and consistent monitoring, errors caught more reliably

- Intelligent – continuous analysis, real-time visibility, and scenario-driven decisions that inform bank relationship strategy.

The meaningful gains come at the final stage, where fee management becomes proactive rather than retrospective. Organisations that reach it typically identify savings equivalent to 10–15%3 of their total annual bank fee spend. For a group with significant banking relationships, that is not a marginal gain.

The gains come from three consistent sources: eliminating billing errors and redundant charges, removing unused services and accounts, and renegotiating pricing from a position of data rather than assumption.

Why it matters beyond cost reduction

Sustained fee management changes more than the cost line. When you understand how balances, services, and pricing interact across your banking panel, liquidity allocation decisions become better informed.

When you can demonstrate line-by-line what you are paying and why, bank relationship reviews and RFP processes shift from negotiation by instinct to negotiation by evidence.

And when you have continuous visibility over a cost category that was previously opaque, the dynamic with your banks changes entirely. You are no longer a passive recipient of a bill. You are a counterparty with data.

Bank fees will always exist. The question is whether your treasury function has the infrastructure to understand and manage them continuously, or whether value continues to leave quietly in the background.

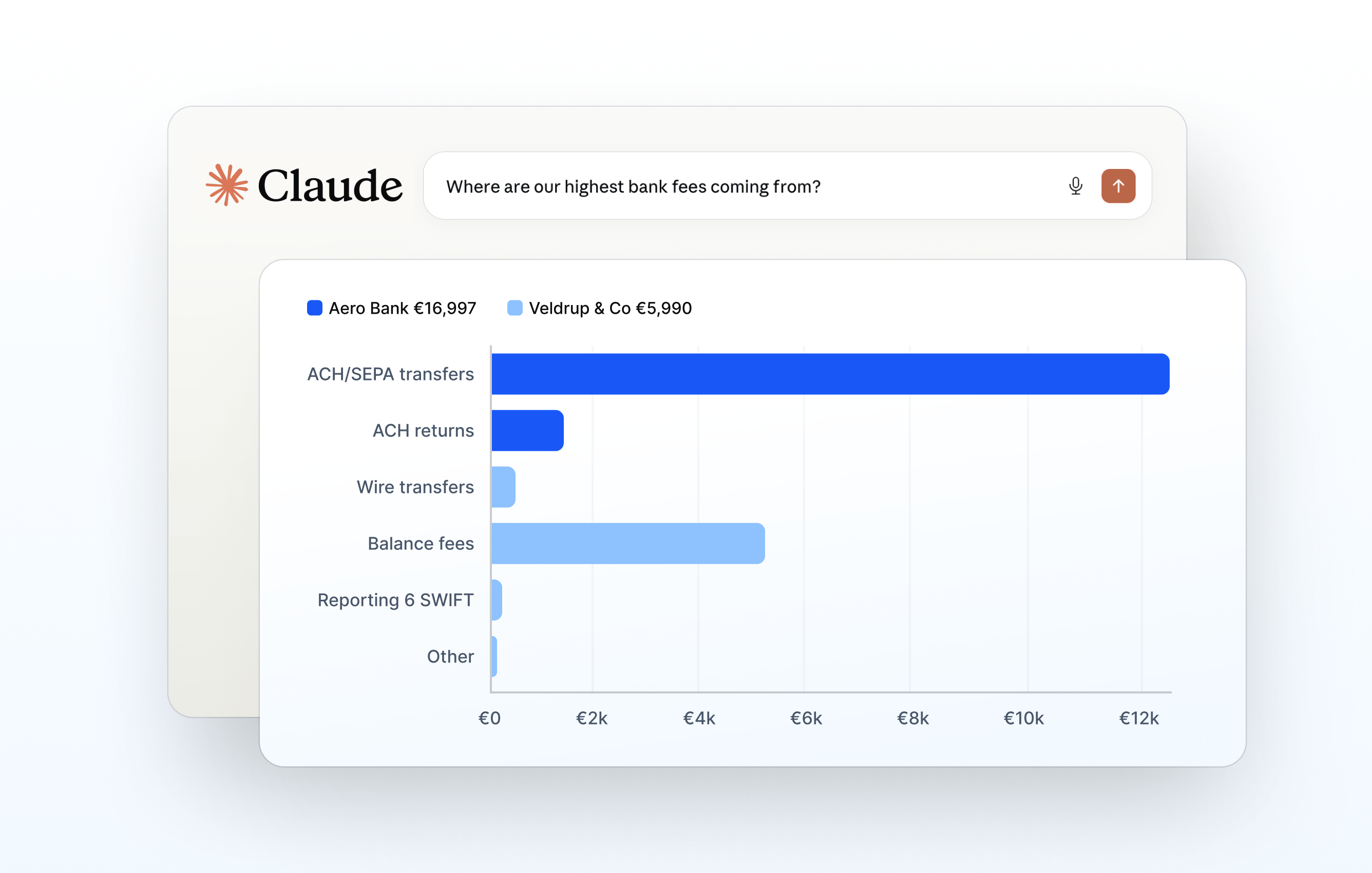

The role of connected AI

With FinanceKey’s MCP server now available, getting a grip on bank fees has becomee considerably more straightforward. Connect your AI assistant directly to live fee data, ask the questions you have always wanted to ask, and get answers without building a report first.

The infrastructure that makes real treasury AI possible is the same infrastructure that makes bank fee intelligence actionable. We have built both.

If you would like to see how it works, get in touch.

References

- McKinsey Global Payments Report

- Medius AP Automation Benchmarks

- EY Bank Fee Optimisation.