Cash flow forecasting: From spreadsheets to programmable liquidity

By Veikko Koski, Co-Founder, FinanceKey

Cash flow forecasting remains one of the most persistent pain points in treasury. At a time when finance is moving toward real-time data, API connectivity, and automation, forecasting should be getting easier. Instead, most teams are still building forecasts from spreadsheets and manual inputs, held back by fragmented processes and disconnected systems.

The good news is that the path forward is clearer than it might seem.

In this article I look at why forecasting is fundamentally a coordination challenge, what better looks like across different time horizons, and how the combination of real-time connectivity and AI is making a more automated, more reliable approach possible – for teams at every stage of maturity.

The challenge: coordinating forecasting inputs

Forecasting is often treated as a modelling problem. In reality, most teams never get that far.

The data exists. The challenge is that it sits in different systems, owned by different teams, and becomes visible too late. Treasury, AP, AR, FP&A, and local finance teams all hold pieces of the picture – each with their own assumptions and level of detail.

The result is a process built around chasing inputs, aligning formats, and resolving inconsistencies. By the time the data is aligned and aggregated, the situation has already changed.

Improving the model does not solve this. Better coordination does.

This is also why Excel persists. It is not good at forecasting. But it is flexible, familiar, and available to everyone. Most systems cannot match that.

Excel survives not because it is good, but because everything else is harder.

Three horizons, three different problems

Cash flow forecasting is often treated as one problem. In reality, it consists of very different challenges depending on the time horizon.

- In the short term – typically up to 30 days – forecasting is about liquidity management. The focus is on making sure cash is in the right place, at the right time, and in the right currency. Timing differences have real operational impact.

- In the mid-term, roughly 30 to 90 days, the challenge shifts to coordination. Inputs come from different teams, business units, and assumptions. Accuracy is less about exact timing and more about having a reliable, aligned view of upcoming cash positions – and planning investment and funding activities accordingly.

- In the long term, from 3 to 12 months, forecasting becomes strategic. The focus is on planning, scenario analysis, and supporting decision-making. Direction matters more than precision.

The most operational pressure sits in the short term. This is where timing, visibility, and execution come together – and where current processes break down the most.

For smaller organisations, short-term liquidity often sits with the CFO: understanding whether upcoming outflows can be covered and whether funding needs to be arranged. For larger organisations, treasury teams manage this centrally, often across multiple entities and hundreds of bank accounts.

In my previous experience managing liquidity in a large, centralised treasury setup, visibility to payment outflows was the key enabler. When all payments were centrally managed and visible in advance, the short-term liquidity position became highly predictable. Cash could be moved proactively to where it was needed, and excess liquidity could be centralised and allocated more efficiently within defined risk limits.

In many organisations, that level of visibility is still missing.

Case study

Nors drives €1M+ in treasury savings with FinanceKey

Find out how Nors moved to real-time liquidity management, enabled by API-based bank connectivity and automated sweeps.

Programmable liquidity: a glimpse of what’s possible

At the leading edge of short-term liquidity management, a very different model is emerging.

In a recent conversation I had with a large multinational corporate, the concept of “programmable bank accounts” came up.

In this model, liquidity management is largely automated: balances are monitored in real time, rules trigger fund movements automatically, overdrafts are covered without manual intervention, and excess cash is centralised continuously.

The technology behind this is not complex in principle – real-time balance visibility via APIs, combined with centralised control over payments. This is the model FinanceKey is built on – API-first, real-time balance reporting and centralised payment visibility, typically live in weeks.

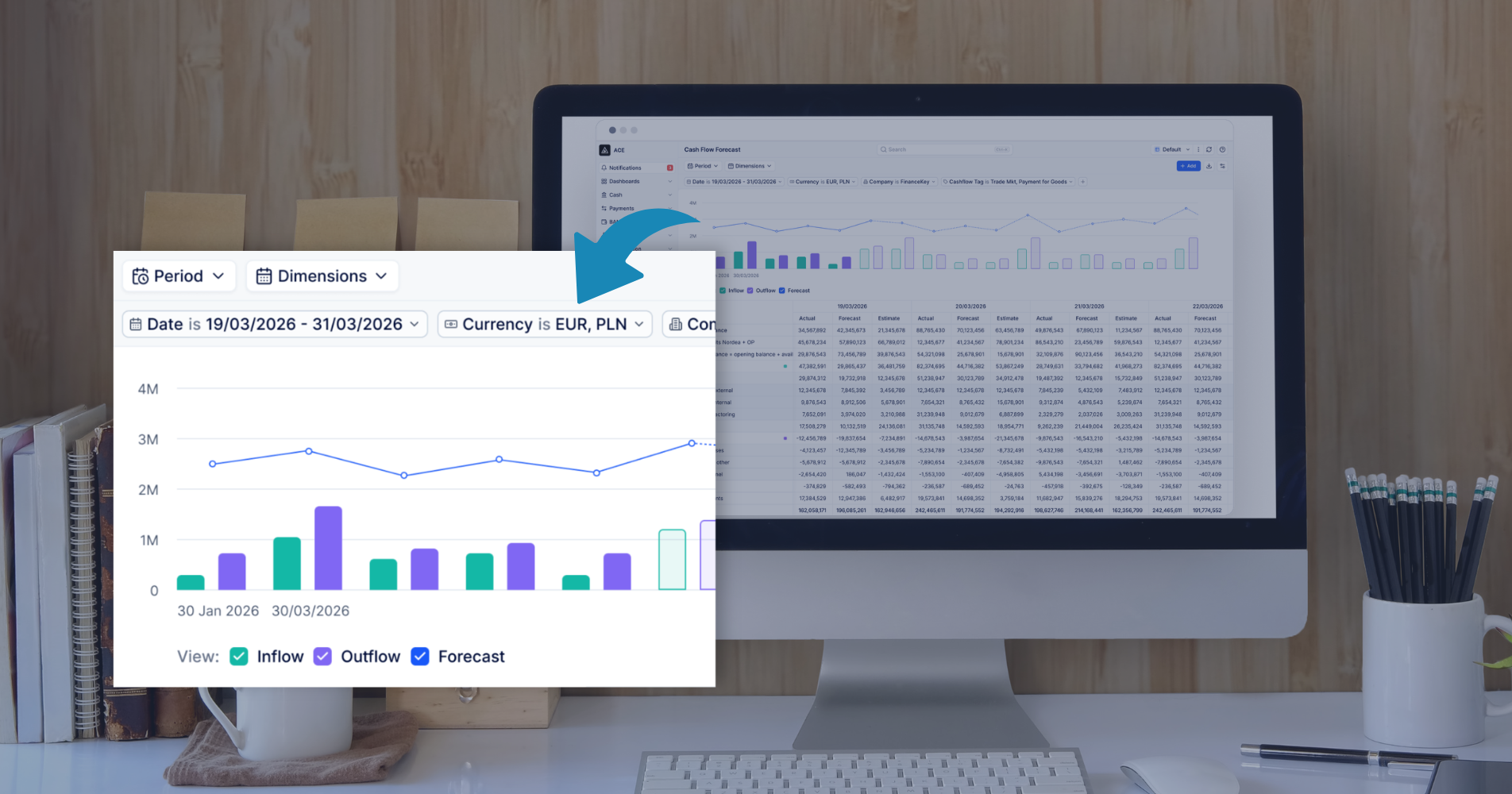

When you can see every payment – by entity, currency, and bank account – and monitor positions in real time, the role of forecasting changes. It becomes less about predicting cash positions and more about orchestrating them.

Many of the coordination challenges described earlier start to disappear. Visibility is no longer delayed. Payment timing is known. Liquidity decisions can be automated.

This also requires a shift in mindset. For many CFOs, end-of-day visibility is still sufficient. Moving to real-time means trusting automated processes and operating with a much shorter decision cycle.

Where AI actually helps

AI is often positioned as a way to improve forecast accuracy. In practice, its biggest impact is earlier in the process, for teams still working through the coordination challenges above.

It helps with data preparation – standardising inputs that arrive in inconsistent formats, flagging gaps, reducing manual effort before the data can be used. It simplifies how people interact with forecasting systems, allowing natural language queries and reducing reliance on complex interfaces. And it strengthens the feedback loop between forecast and actuals, helping teams understand where assumptions need to improve.

AI also supports with pattern recognition and trend identification from historical data, helping to build future estimates. But this only applies when the underlying data and processes are already in reasonable shape.

AI does not remove the need for coordination. It makes coordination easier.

Fix the input problem first

If forecasting is a coordination problem, the solution starts with making inputs and data aggregation easy. Interfaces should be intuitive to use. APIs and integrations should automate data flows where possible. Where needed, Excel can still be one way to collect data.

Human inputs, system data, and bank data should come together in a single view.

Once the data foundation is in place, modelling becomes worthwhile. AI helps with both: cleaning and structuring data on one side, and building forecasting models – identifying patterns, seasonality, and trends from historical data – on the other.

If you are struggling with cash flow forecasting, let’s talk.